10-K: Annual report pursuant to Section 13 and 15(d)

Published on

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☑ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE

SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2017

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d)

OF

THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File No.:001-34079

Rexahn Pharmaceuticals, Inc.

(Exact name of registrant as specified in its charter)

|

Delaware

|

11-3516358

|

|

|

(State or other jurisdiction of incorporation or organization)

|

(I.R.S. Employer Identification Number)

|

15245 Shady Grove Road, Suite 455

Rockville, MD 20850

(Address of principal executive offices, including zip code)

Telephone: (240) 268-5300

(Registrant’s telephone number, including area code)

|

Title of Each Class

|

Name of Each Exchange On Which Registered

|

|

|

Common Stock, $0.0001 par value per share

|

NYSE American

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined by Rule-405 of the Securities Act. Yes ☐ No ☑

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act.

Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☑ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein; and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☑

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definition of “accelerated filer,” “large accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large Accelerated Filer

|

☐

|

Accelerated Filer

|

☑

|

|

Non-Accelerated Filer

|

☐

|

Smaller reporting company

|

☐

|

|

(Do not check if a smaller reporting company)

|

Emerging growth company

|

☐

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) Yes ☐ No ☑

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter: As of June 30, 2017, the aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was $79,303,524 based on the closing price reported on NYSE American.

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date:

|

Class

|

Outstanding as of March 9, 2018

|

|

|

Common Stock, $0.0001 par value per share

|

31,744,439 shares

|

DOCUMENTS INCORPORATED BY REFERENCE

Certain portions of the registrant’s Definitive Proxy Statement for its 2018 Annual Meeting of Stockholders, which is expected to be filed with the U.S. Securities and Exchange Commission within 120 days after the end of the registrant’s fiscal year ended December 31, 2017, are incorporated by reference into Part III of this Annual Report on Form 10-K.

Cautionary Statement Regarding Forward-Looking Statements.

This Annual Report on Form 10‑K contains statements (including certain projections and business trends) accompanied by such phrases as “believe,” “estimate,” “expect,” “anticipate,” “will,” “intend” and other similar expressions, that are “forward-looking statements” as defined in the Private Securities Litigation Reform Act of 1995. We caution that forward-looking statements are based largely on our expectations and are subject to a number of known and unknown risks and uncertainties that are subject to change based on factors that are, in many instances, beyond our control. Actual results, performance or achievements may differ materially from those contemplated, expressed or implied by the forward-looking statements.

Although we believe that the expectations reflected in our forward-looking statements are reasonable as of the date we make them, actual results could differ materially from those currently anticipated due to a number of factors, including risks relating to:

| · |

our understandings and beliefs regarding the role of certain biological mechanisms and processes in cancer;

|

| · |

our drug candidates being in early stages of development, including in pre-clinical development;

|

| · |

our ability to initially develop drug candidates for orphan indications to reduce the time-to-market and take advantage of certain incentives provided by the U.S. Food and Drug Administration;

|

| · |

our ability to transition from our initial focus on developing drug candidates for orphan indications to candidates for more highly prevalent indications;

|

| · |

our ability to successfully and timely complete clinical trials for our drug candidates in clinical development;

|

| · |

uncertainties related to the timing, results and analyses related to our drug candidates in pre-clinical development;

|

| · |

our ability to obtain the necessary U.S. and international regulatory approvals for our drug candidates;

|

| · |

our reliance on third-party contract research organizations and other investigators and collaborators for certain research and development services;

|

| · |

our ability to maintain or engage third-party manufacturers to manufacture, supply, store and distribute supplies of our drug candidates for our clinical trials;

|

| · |

our ability to form strategic alliances and partnerships with pharmaceutical companies and other partners for sales and marketing of certain of our product candidates;

|

| · |

demand for and market acceptance of our drug candidates;

|

| · |

the scope and validity of our intellectual property protection for our drug candidates and our ability to develop our candidates without infringing the intellectual property rights of others;

|

| · |

our lack of profitability and the need for additional capital to operate our business; and

|

| · |

other risks and uncertainties, including those set forth herein under the caption “Risk Factors” and those detailed from time to time in our filings with the Securities and Exchange Commission.

|

These forward-looking statements are made only as of the date hereof, and we undertake no obligation to update or revise the forward-looking statements, whether as a result of new information, future events or otherwise.

REXAHN PHARMACEUTICALS, INC.

|

Page

|

|||

|

PART I

|

1

|

||

|

Item 1

|

1

|

||

|

Item 1A

|

24

|

||

|

Item 1B

|

43

|

||

|

Item 2

|

43

|

||

|

Item 3

|

43

|

||

|

Item 4

|

43

|

||

|

PART II

|

44

|

||

|

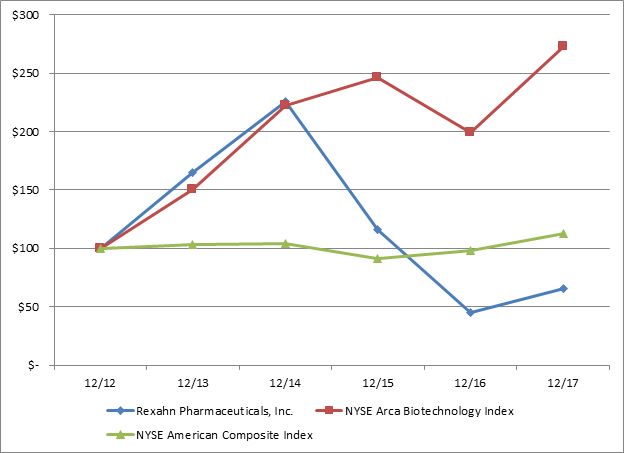

Item 5

|

44

|

||

|

Item 6

|

46

|

||

|

Item 7

|

47

|

||

|

Item 7A

|

59

|

||

|

Item 8

|

59

|

||

|

Item 9

|

60

|

||

|

Item 9A

|

60

|

||

|

Item 9B

|

62

|

||

|

PART III

|

63 | ||

|

Item 10

|

63

|

||

|

Item 11

|

63

|

||

|

Item 12

|

63

|

||

|

Item 13

|

63

|

||

|

Item 14

|

63

|

||

|

Item 15

|

64

|

||

|

Item 16

|

64

|

||

|

69

|

|||

PART I

Unless the context requires otherwise, any references in this Annual Report on Form 10-K to “we,” “us,” “our,” the “Company” or “Rexahn” refers to Rexahn Pharmaceuticals, Inc.

Overview

We are a clinical stage biopharmaceutical company dedicated to the discovery and development of innovative treatments for cancer. Our mission is to improve the lives of cancer patients by developing next-generation cancer therapies that are designed to maximize efficacy while minimizing the toxicity and side effects traditionally associated with cancer treatment. Our pipeline features two oncology product candidates in Phase 2 clinical development and additional compounds in pre-clinical development. Our strategy is to continue building a significant pipeline of innovative oncology product candidates that we intend to commercialize with partners. Our clinical stage drug candidates in active development are RX-3117 and RX-5902 (Supinoxin™).

| · |

RX-3117 is a novel, oral, small molecule nucleoside compound. Once intracellularly activated (phosphorylated) by the enzyme UCK2, it is incorporated into the DNA or RNA of cells and inhibits both DNA and RNA synthesis, which induces apoptotic cell death of tumor cells. Because UCK2 is overexpressed in multiple human tumors, but has a very limited presence in normal tissues, RX-3117 offers the potential for a targeted anti-cancer therapy with an improved efficacy and safety profile, and we believe it has therapeutic potential in a broad range of cancers, including pancreatic, bladder, colon, and lung cancer. In January 2018, we reported final data from a Phase 2a clinical trial of RX-3117 in patients with relapsed or refractory metastatic pancreatic cancer. In this trial, encouraging progression free survival and evidence of tumor shrinkage were observed in patients with metastatic pancreatic cancer that was resistant to gemcitabine and who had failed on multiple prior treatments. RX-3117 is currently the subject of a Phase 2a clinical trial in combination with Abraxane® (paclitaxel protein-bound) in patients newly diagnosed with metastatic pancreatic cancer. In February 2018, updated safety and efficacy data from the ongoing Phase 2a clinical trial of RX-3117 in advanced urothelial (bladder) cancer were reported. In this trial, encouraging progression free survival and evidence of tumor shrinkage were observed in patients with advanced bladder cancer who had failed on multiple prior treatments including immunotherapy and gemcitabine. RX-3117 has received “orphan drug designation” from the U.S. Food and Drug Administration (“FDA”) and from the European Commission (“EC”) for pancreatic cancer. Orphan drug designation in the U.S. provides tax incentives for clinical research and a waiver from user fees under certain circumstances. In addition, an orphan drug generally receives seven years of exclusivity in the U.S. after approval for a designated use, during which time the FDA generally cannot approve another product with the same active moiety for the same indication.

|

| · |

RX-5902 (Supinoxin) is a potential first-in-class small molecule inhibitor of phosphorylated-p68, a protein that we believe plays a key role in cancer cell growth, progression and metastasis through its interaction with beta-catenin. Phosphorylated p68, which is highly expressed in cancer cells, but not in normal cells, results in up-regulation of cancer-related genes and a subsequent proliferation of cancer cells and tumor growth. RX-5902 selectively blocks the interaction of phosphorylated p68 with beta-catenin, thereby decreasing the proliferation or growth of cancer cells in preclinical models. In addition, multiple pre-clinical models suggest that RX-5902 enhances the efficacy of immunotherapy. We have evaluated RX-5902 in a Phase 1 dose escalation study in patients with a diverse range of metastatic, treatment-refractory tumors, including breast, ovarian, colorectal, and neuro-endocrine tumors. In February 2017, we initiated a Phase 2a clinical study of RX-5902 in patients with metastatic triple negative breast cancer (“TNBC”).

|

| · |

RX-0201 (Archexin) is a potential best-in-class, potent inhibitor of the protein kinase Akt-1, which we believe plays a critical role in cancer cell proliferation, survival, angiogenesis, metastasis and drug resistance. RX-0201 is the subject of a research and development collaboration with Zhejiang Haichang Biotechnology Co., Ltd. (“Haichang”) for the development of RX-0201 to conduct certain pre-clinical and clinical activities through completion of a Phase 2a proof-of-concept clinical trial in hepatocellular carcinoma (“HCC”) and pursuant to which the parties will share any downstream licensing fees and royalties paid by third parties in connection with the further development and commercialization of RX-0201 for the treatment of HCC. RX-0201 has received orphan drug designation from the FDA for renal cell carcinoma (“RCC”), glioblastoma, ovarian cancer, stomach cancer and pancreatic cancer. In February 2018, in response to the changing treatment landscape for metastatic RCC over the past two years with the approval of new therapies by the FDA, we announced plans to discontinue the internally funded programs of RX-0201 and ceased enrolling patients in a Phase 2a proof-of-concept clinical trial of RX-0201 in patients with metastatic renal cell carcinoma.

|

In addition to our drug development efforts, our nano-based drug delivery systems, such as those used in the multiple nanoliposomal- and nanopolymer-based anti-cancer drugs that we are currently testing, may increase the availability of a drug at the disease site, minimize adverse reactions, and provide longer duration of action.

Company Background

We trace our history to the March 2001 founding of Rexahn, Corp. Dr. Peter D. Suzdak, our Chief Executive Officer since February 2013, has extensive experience in corporate management and drug development, particularly in the field of oncology.

Our common stock is currently listed on the NYSE American under the trading symbol “RNN.” Our principal corporate office is located at 15245 Shady Grove Road, Suite 455, Rockville, Maryland 20850 in Maryland’s I-270 technology corridor. Our telephone number is (240) 268-5300.

Industry and Disease Markets

Market Overview

Our primary research and development focus is oncology therapeutics. A key component of our strategy is to develop innovative drugs that are potential first-in-class or market-leading compounds for the treatment of cancer. According to the Centers for Disease Control and Prevention, cancer claims the lives of more than half a million Americans each year and is the second leading cause of death among Americans. The World Health Organization estimated in 2018 that there were 14 million new cases of cancer diagnosed worldwide in 2012 and that cancer was responsible for 8.8 million deaths in 2015. A 2018 American Cancer Society report projected that an estimated 1.7 million new cancer cases will be diagnosed in the United States in 2018. The IQVIA Institute for Human Data Science, formerly the IMS Institute for Healthcare Informatics, reported in 2017 that total global spending on oncology medicines, including therapeutic treatments and supportive care, reached $113 billion in 2016.

Current Cancer Treatments

Traditional cancer treatments involve surgery, radiation therapy and chemotherapy. Surgery is widely used to treat cancer but may result in related or significant complications and may be ineffective if metastasis has occurred. Radiation therapy, or radiotherapy, can be highly effective in treating certain types of cancer. In radiation therapy, ionizing radiation deposits energy that injures or destroys cells in the area being treated by damaging their genetic material, making it impossible for these cells to continue to grow. Although radiation damages both cancer cells and normal cells, the normal cells are generally able to repair themselves and function properly. Chemotherapy involves the use of cytotoxic cancer drugs to destroy cancer cells by interfering with various stages of the cell division process. For certain cancers and in certain patients, these drugs have limited efficacy and debilitating adverse side effects. Administration of generally cytotoxic cancer drugs may also result in the development of multi-drug resistance, a condition that results when certain tumor cells that have survived treatment with cytotoxic drugs are no longer susceptible to treatment by those and other drugs. Recent advances in cancer treatment include the use of cancer-targeted cytotoxic agents and immunotherapies to stimulate the body’s own immune system to kill cancer cells. Immunotherapy can significantly improve survival in certain cancers, including melanoma, non-small cell lung cancer, head and neck tumors, lymphoma and renal cell carcinoma. However, immunotherapy approaches have not been effective in all tumor types and there is a risk of over-stimulation of the immune system that can lead to life-threatening autoimmune side-effects, such as colitis, pneumonia, and hepatitis.

Unmet Needs in Cancer

Despite significant advances in cancer research and treatments, many unmet needs still remain including:

| · |

Long-term management of cancers: Surgery, radiation therapy or chemotherapy may not result in long-term remission, although surgery and radiation therapies are considered effective methods for some cancers. There is a need for more effective drugs and adjuvant therapies to treat relapsed and refractory cancers.

|

| · |

Multi-drug resistance: Multi-drug resistance is a major obstacle to effectively treating various cancers with chemotherapy.

|

| · |

Debilitating toxicity by chemotherapy: Chemotherapy as a mainstay of cancer treatment can induce severe adverse reactions and toxicities, adversely affecting quality of life or life itself.

|

Market Opportunity

There are several factors that we believe are favorable for commercializing new cancer drugs that may have the potential to be first-in-class or market leaders, including:

| · |

Expedited Regulatory or Commercialization Pathways. Drugs for life-threatening diseases such as cancer are often candidates for fast track designation, breakthrough therapy designation, priority review and accelerated approval, each of which may lead to approval sooner than would otherwise be the case.

|

| · |

Favorable Environment for Formulary Access and Reimbursement. We believe cancer drugs with proven efficacy would gain rapid market uptake, formulary listing and third-party payor reimbursement. Drugs with orphan designations are generally reimbursed by third-party payors because there are few, if any, alternatives.

|

| · |

Low Marketing Costs. We believe the marketing of new drugs to oncologists can be accomplished with a smaller sales force and lower related costs than a sales force that markets widely to primary care physicians and general practitioners.

|

Our Strategy

Our strategy is to continue building a significant product pipeline of innovative drug candidates that we intend to commercialize alone or with partners. This strategy has several key components.

Develop Innovative Therapeutics with the Potential to be First-in-Class or Market Leaders

We plan to focus our research and development pipeline on potential first-in-class or market-leading compounds for the treatment of cancer. By expanding the breadth and depth of our oncology pipeline, we aim to develop an industry-leading oncology therapeutics franchise. Our pipeline spans several major classes of cancer drugs, including molecular targeted therapies and nano-medicines for targeted delivery of compounds and small molecule cytotoxic compounds. Differentiated target product profiles and proprietary discovery and research technology platforms further support these strategic efforts.

Clinically Develop Drug Candidates as Orphan Drugs in Underserved Specialty Oncology Indications

We intend to initially develop drug candidates for cancers that are orphan indications or for indications where there has been very little innovation and a high unmet need for better treatments. Under the Orphan Drug Act, the FDA may grant orphan drug designation to new drugs developed to treat diseases generally affecting less than 200,000 patients. Benefits associated with orphan drug designation include tax incentives for research and development and an exemption from user fees under certain circumstances. Although the standards for orphan drug approval are not different than for non-orphan products, the path to approval may be faster because clinical trials may be smaller due to the smaller patient population. Further, a drug that is approved for its orphan-designated indication generally receives seven years of orphan drug exclusivity, during which the FDA generally may not approve any other application for a product containing the same active moiety and proposed for the same indication. An approved orphan drug also may qualify for an exemption from the branded prescription drug fee. The European Union (“EU”) also has a version of orphan drug designation, which generally carries with it a ten-year period of market exclusivity. We plan to develop drug candidates, when possible, for cancers that are orphan indications to take advantage of the benefits of orphan drug designation during development and the exclusivity available under applicable law for approved products, as well as the potential for reduced time to market. Assuming positive clinical data, drugs intended to treat rare diseases or conditions also may qualify for fast track designation, breakthrough therapy designation, accelerated approval or priority review, any or all of which may speed the development and approval process and decrease drug development costs.

Establish Partnerships with Large Pharmaceutical Companies

We seek to establish strategic alliances and partnerships with larger pharmaceutical companies for the commercialization and co-development of our drug candidates.

In-License Unique Technology

We continually review opportunities to in-license and advance compounds in oncology that have value-creating potential and will strengthen our clinical development pipeline.

Capitalize on Our Management Team’s Expertise for Drug Development

Our management team possesses clinical development experience in oncology and several other therapeutic areas which facilitates strategic approaches to and competitive advantages in, the design, risk assessment and implementation of drug development programs. Our management team also has prior experience in pharmaceutical alliances, product launches and marketing.

Our Pipeline Drug Candidates

Clinical Stage Pipeline

RX-3117: Oral Small Molecule Nucleoside

RX-3117 is a novel, investigational, oral small molecule nucleoside compound. In pre-clinical models when activated (phosphorylated) by uridine-cytidine kinase 2, a protein that is overexpressed in various human cancer cells, RX-3117 is incorporated into DNA or RNA of cells and inhibits both DNA and RNA synthesis, which induces apoptotic cell death of tumor cells. We believe RX-3117 has therapeutic potential in a broad range of cancers including pancreatic, bladder, lung, cervical, non-small cell lung cancer and colon cancer. RX-3117 has received orphan drug designation from the FDA and the EC for the treatment of patients with pancreatic cancer. RX-3117 has also been shown in animal models to inhibit the growth of gemcitabine-resistant human cancers and improve overall survival.

RX-3117 has demonstrated broad spectrum anti-tumor activity against over 100 different human cancer cell lines and efficacy in 17 different mouse xenograft models. Notably, the efficacy of RX-3117 in the mouse xenograft models was superior to that of gemcitabine. Further, RX-3117 still retains its full anti-tumor activity in human cancer cell lines made resistant to the anti-tumor effects of gemcitabine. In August 2012, we reported the completion of an exploratory Phase 1 clinical trial of RX-3117 in cancer patients conducted in Europe to investigate the oral bioavailability, safety and tolerability of the compound. In this study, oral administration of a 50 mg dose of RX-3117 demonstrated an oral bioavailability of 56% and a plasma half-life (T1/2) of 14 hours. In addition, RX-3117 appeared to be safe and well tolerated in all subjects throughout the dose range tested.

Final results from the Phase 1b clinical trial of RX-3117 presented at the American Society of Clinical Oncology Annual Meeting in June 2016 showed evidence of single agent activity. Patients in the study had generally received four or more cancer therapies prior to enrollment. In this study, 12 patients experienced stable disease persisting for up to 276 days and three patients showed evidence of tumor burden reduction. A maximum tolerated dose of 700 mg was identified in the study. At the doses tested to date, RX-3117, administered orally, appeared to be safe and well tolerated with a predictable pharmacokinetic profile following oral administration.

In March 2016, we initiated a multi-center Phase 2a clinical trial of RX-3117 in patients with relapsed or refractory pancreatic cancer to further evaluate the safety and anti-cancer properties of this compound. Patients in the trial received a 700 mg daily oral dose of RX-3117, for five consecutive days, followed by two days off, for three weeks, followed by a week of rest, in a 28-day cycle for up to eight treatment cycles, or until their disease progressed. The study was designed as a two-stage study with 10 patients in stage 1 and an additional 40 patients in stage 2. According to pre-set criteria, if greater than 20% of the patients had an increase in progression free survival of more than four months, or an objective clinical response rate and reduction in tumor size, additional pancreatic cancer patients would be enrolled into stage 2. Secondary endpoints included time to disease progression, overall response rate and duration of response, as well as pharmacokinetic assessments and safety parameters.

In September 2016, we initiated stage 2 of this Phase 2a clinical trial based on the satisfaction of the predefined criteria for preliminary efficacy for stage 1 of the trial that showed RX-3117 was safe and well tolerated with preliminary efficacy in pancreatic cancer patients for whom three or more prior therapies had been ineffective. In January 2018, we presented the final data from this trial at the American Society of Clinical Oncology Gastrointestinal Cancers 2018 Annual Meeting. Encouraging progression free survival and evidence of tumor shrinkage was observed in patients with metastatic pancreatic cancer resistant to gemcitabine who had failed on multiple prior treatments.

In November 2017, we initiated a Phase 2a trial of RX-3117 in combination with Abraxane® in patients newly diagnosed with metastatic pancreatic cancer.

In September 2016, we commenced enrollment in a Phase 2a trial of RX-3117 in patients with advanced bladder cancer. This Phase 2a clinical trial is a multicenter, open-label, single-agent study of RX-3117 being conducted at 10 clinical centers in the United States. RX-3117 is being administered orally five times weekly on a three weeks on, one week off dosing schedule. The primary endpoint for the trial is an assessment of the progression free survival rate or an objective clinical response rate and reduction in tumor size. Secondary endpoints include time to disease progression, overall response rate and duration of response, as well as pharmacokinetic assessments and safety. In February 2018, we presented data from this trial at the American Society of Clinical Oncology Genitourinary Cancers 2018 Annual Meeting. Encouraging progression free survival and evidence of tumor shrinkage were observed in patients with advanced bladder cancer who had failed on multiple prior treatments including immunotherapy and gemcitabine.

Based on the progress of the RX-3117 clinical development program, we are continuing discussions with multiple companies to explore collaborative business structures in an effort to maximize the potential value of the program.

RX-5902 (Supinoxin): Potential First-in-Class Inhibitor of Phosphorylated p68

RX-5902 is a potential first-in-class small molecule inhibitor of the interaction between phosphorylated-p68, a protein that we believe plays a key role in cancer growth, progression and metastasis and beta-catenin. Many cancers are driven by beta-catenin-mediated gene expression. Phosphorylated p68, which is highly expressed in cancer cells, but not in normal cells, results in up-regulation of cancer-related genes and a subsequent proliferation of cancer cells and tumor growth. RX-5902 selectively blocks the phosphorylated p68-beta catenin interaction, thereby decreasing the proliferation or growth of cancer cells. In pre-clinical tissue culture models and in-vivo xenograft models, RX-5902 has exhibited single-agent tumor growth inhibition, potential synergy with cytotoxic agents and activity against drug resistant cancer cells. In particular, in in-vivo xenograft models of human triple negative breast cancer and pancreatic cancer, treatment with RX-5902 on days one through 20 in mouse models produced a dose-dependent inhibition of tumor growth and a survival benefit.

RX-5902 was evaluated in a Phase 1 dose-escalation clinical trial in cancer patients with solid tumors designed to evaluate the safety, tolerability, dose-limiting toxicities and the recommended Phase 2 dose. Secondary endpoints include pharmacokinetic analyses and an evaluation of the preliminary anti-tumor effects of RX-5902. We completed enrollment in this study in 2016.

Updated results from the Phase 1 clinical trial of RX-5902 were presented in October 2016 at the 2016 European Society for Medical Oncology Congress.

The results showed evidence of single-agent, clinical activity of RX-5902. In this study, RX-5902 preliminarily appeared to be safe and well tolerated at the doses and dosing schedules tested with no dose limiting toxicities or treatment-related serious adverse events. The most frequently reported drug related adverse events were mild nausea, vomiting and fatigue. Initial signs of clinical activity have been observed. Twenty-four subjects were enrolled (11 female, 13 male), and seven subjects experienced stable disease in breast, neuroendocrine, paraganglioma, head/neck or colorectal cancer. Three subjects received treatment for more than one year. Approximately 55% of the subjects had received four or more therapies prior to their enrollment in the Phase 1 clinical study.

We initiated a Phase 2a study of RX-5902 in patients with triple negative breast cancer in February 2017. The study will evaluate the safety and preliminary efficacy of RX-5902 in patients with metastatic triple negative breast cancer who have failed prior treatments. We also plan to evaluate RX-5902 in combination with other anticancer agents in TNBC, assuming positive data from this initial study.

Based on the progress of the RX-5902 clinical development program, we are continuing our discussions with multiple companies to explore collaborative business structures in an effort to maximize the potential commercial value of the program.

RX-0201 (Archexin): Potential Best-in-Class Anti-Cancer Akt-1 Inhibitor

RX-0201 is a potential best-in-class, potent anti-sense inhibitor of protein kinase Akt-1 synthesis and activity, which we believe plays a critical role in cancer cell proliferation, survival, angiogenesis, metastasis and drug resistance. RX-0201 has received orphan drug designation from the FDA for RCC, glioblastoma, ovarian cancer, stomach cancer and pancreatic cancer. We believe RX-0201 is differentiated from other Akt-1 inhibitors by its ability to inhibit both activated and inactivated forms of Akt-1, and as a result it is not expected to lead to drug resistance, which has been observed with other protein kinase inhibitors. Other targeted drugs may only inhibit inactivated Akt-1 and may also cause drug resistance. Akt-1 is over-activated in patients with many cancers, including breast, colorectal, gastric, pancreatic, prostate and melanoma cancers. Akt-1 activity may be inhibited by signaling molecules upstream of Akt-1 in cancer cells through the use of vascular endothelial growth factor and epidermal growth factor receptor inhibitors, but this treatment only indirectly affects the activity of native Akt-1. Because signal transmission for cancer progression and resistance occurs when Akt-1 is activated, we believe it is also important to inhibit activated Akt-1. We believe RX-0201 inhibits both activated and native Akt-1.

RX-0201 is an antisense oligonucleotide compound that is complementary to Akt-1 mRNA and highly selective for inhibiting mRNA expression, which leads to reduced production of Akt-1 protein. RX-0201 preliminarily appeared to be safe and well tolerated with minimal side effects in a Phase 1 study in patients with advanced cancers, where Grade 3 fatigue was the only dose-limiting toxicity and no significant hematological abnormalities were observed. A nano-liposomal formulation of RX-0201 is being developed under a collaboration with Haichang using Haichang’s proprietary QTzomes™ technology. Under the agreement, Haichang intends to conduct a Phase 2a proof-of-concept clinical study in HCC in China.

We completed a Phase 2a clinical trial for RX-0201 that was designed to assess the safety and efficacy of RX-0201 in combination with gemcitabine. RX-0201 was shown to be safe and well tolerated with a preliminary indication of activity.

In January 2014, we initiated a Phase 2a proof-of-concept clinical trial of RX-0201 to study its safety and efficacy in combination with Afinitor® (everolimus) in patients with metastatic RCC. The trial is being conducted in two stages. Stage 1 was a dose ranging study, with up to three dose groups with three RCC patients each, to determine its maximum tolerated dose (“MTD”) in combination with everolimus. In January 2016, we completed Stage 1 of the study and commenced enrollment in Stage 2, which is a randomized, open-label, two-arm dose expansion study of everolimus versus RX-0201 in combination with everolimus to determine safety and efficacy of the combination. This phase of the trial (Stage 2) was anticipated to enroll up to 40 RCC patients randomized to receive either RX-0201 in combination with everolimus, or everolimus alone, in a ratio of 2:1 The MTD was determined to be 250 mg/m2/day of RX-0201, which was identified in Stage 1 and was administered in Stage 2 along with 10 mg of everolimus compared to 10 mg everolimus alone. In February 2018, following a portfolio review of assets and in response to the changing treatment landscape for RCC patients over the past two years with the approval of new therapies by the FDA, we announced that we are winding down internally funded programs of RX-0201 including the cessation of enrollment in this trial. Patients currently enrolled in the trial will continue to be followed.

Research and Development Process

We have engaged third-party contract research organizations and other investigators and collaborators, such as universities and medical institutions, to conduct our pre-clinical studies, toxicology studies and clinical trials. Engaging third-party contract research organizations is typical practice in our industry. However, relying on such organizations means that the clinical trials and other studies described above are being conducted at external locations and that the completion of these trials and studies is not within our direct control. Trials and studies may be delayed due to circumstances outside our control, and such delays may result in additional expenses for us.

Competition

We compete against fully integrated pharmaceutical companies and smaller companies that are collaborating with larger pharmaceutical companies, as well as academic institutions, government agencies and other public and private research organizations. Many of these competitors, either alone or together with their collaborative partners, operate larger research and development programs or have substantially greater financial resources than we do, as well as more experience in:

| · |

developing drugs;

|

| · |

undertaking pre-clinical testing and human clinical trials;

|

| · |

obtaining FDA and other regulatory approvals of drugs;

|

| · |

formulating and manufacturing drugs; and

|

| · |

launching, marketing and selling drugs.

|

Large pharmaceutical companies currently sell both generic and proprietary compounds for the treatment of cancer. In addition, companies developing oncology therapies represent substantial competition. Many of these organizations have substantially greater capital resources, larger research and development staff and facilities, history in obtaining regulatory approvals and greater manufacturing and marketing capabilities than we do. These organizations also compete with us to attract qualified personnel, parties for acquisitions, joint ventures or other collaborations.

We are aware of products under development by our competitors that target the same indications as our clinical stage drug candidates. If approved, RX-3117 could compete with other compounds with an anti-metabolite mechanism of action in cancers, such as NUC-1301 (Acelarin®), which is under development by NuCana and other approved nucleoside analogues such as capecitabine and gemcitabine. We are not currently aware of known inhibitors of phosphorylated p68 that would compete with RX-5902 if RX-5902 were approved, but other drugs with a different mechanism of action are in development for the same indications, such as Immunomedics’ sacitazumab govitecan and Celldex’s glembatumumab vedotin, both in development for triple negative breast cancer. Our competitors may succeed in developing products that are safer and/or more effective than ours, which could render our product candidates less competitive prior to recovery by us of expenses incurred with respect to their development.

Government Regulation

Regulation by governmental authorities in the United States and in other countries is a significant consideration in our product development, manufacturing and, upon approval of our product candidates, marketing strategies. We expect that all our drug candidates will require regulatory approval by the FDA and by similar regulatory authorities in foreign countries prior to commercialization and will be subjected to rigorous pre-clinical, clinical, and post-approval testing to demonstrate safety and effectiveness, as well as other significant regulatory requirements and restrictions in each jurisdiction in which we would seek to market our products. U.S. federal laws and regulations govern the testing, development, manufacture, quality control, safety, effectiveness, approval, storage, labeling, record keeping, reporting, distribution, import, export and marketing of all biopharmaceutical products intended for therapeutic purposes. We believe that we and the third parties that work with us are in compliance in all material respects with currently applicable rules and regulations, however, any failure to comply could have a material negative impact on our ability to successfully develop and commercialize our products, and therefore on our financial performance. In addition, these rules and regulations are subject to change. For example, in December 2016, the 21st Century Cures Act (the “Cures Act”) was signed into law. The Cures Act included numerous provisions that may be relevant to our product candidates, including provisions designed to speed development of innovative therapies and provide funding for certain cancer-related research and technology development. Because the Cures Act is still relatively new, it is difficult to foresee whether, how, or when it may affect our business. Further legislative and regulatory changes appear possible in the 115th United States Congress and under the Trump Administration, and it is difficult to foresee whether, how, or when such changes may affect our business.

Obtaining governmental approvals and maintaining ongoing compliance with applicable regulations are expected to require the expenditure of significant financial and human resources not currently at our disposal. We plan to fulfill our short-term needs through consulting agreements and joint ventures with academic or corporate partners while developing our own internal infrastructure for long-term corporate growth.

Development and Approval

The process to obtain approval for biopharmaceutical compounds for commercialization in the United States and many other countries is lengthy, complex and expensive, and the outcome is far from certain. Although foreign requirements for conducting clinical trials and obtaining approval may be different than in the United States, they often are equally rigorous and the outcome cannot be predicted with confidence. A key component of any submission for approval in any jurisdiction is pre-clinical and clinical data demonstrating the product’s safety and effectiveness.

Pre-clinical Testing. Before testing any compound in humans in the United States, a company must develop pre-clinical data, generally including laboratory evaluation of product chemistry and formulation, as well as toxicological and pharmacological studies in animal species to assess safety and quality. Certain types of animal studies must be conducted in compliance with the FDA’s Good Laboratory Practice regulations and the Animal Welfare Act, which is enforced by the Department of Agriculture.

IND Application. In the United States, FDA regulations require that the person or entity sponsoring or conducting a clinical study for the purpose of investigating a candidate’s safety and effectiveness submit to the FDA an investigational new drug (“IND”) application, which contains pre-clinical testing results and provides a basis for the FDA to conclude that there is an adequate basis for testing the drug in humans. If the FDA does not object to the IND application within 30 days of submission, the clinical testing proposed in the IND may begin. Even after the IND has gone into effect and clinical testing has begun, the FDA may put the clinical trials on “clinical hold,” suspending (or in some cases, ending) them because of safety concerns or for other reasons.

Clinical Trials. Clinical trials involve administering a drug to human volunteers or patients under the supervision of a qualified clinical investigator. Clinical trials are subject to extensive regulation. In the United States, this includes compliance with the FDA’s bioresearch monitoring regulations and Good Clinical Practice (“GCP”) requirements, which establish standards for conducting, recording data from, and reporting the results of, clinical trials, with the goal of assuring that the data and results are credible and accurate and that study participants’ rights, safety and well-being are protected. Each clinical trial must be conducted under a protocol that details the study objectives, parameters for monitoring safety and the efficacy criteria, if any, to be evaluated. The protocol is submitted to the FDA as part of the IND and reviewed by the agency before the study begins. Additionally, each clinical trial must be reviewed, approved and conducted under the auspices of an Institutional Review Board (“IRB”). The sponsor of a clinical trial, the investigators and IRBs each must comply with requirements and restrictions that govern, among other things, obtaining informed consent from each study subject, complying with the protocol and investigational plan, adequately monitoring the clinical trial, and timely reporting adverse events. Foreign studies conducted under an IND must meet the same requirements applicable to studies conducted in the United States. However, if a foreign study is not conducted under an IND, the data may still be submitted to the FDA in support of a product application, if the study was conducted in accordance with GCP and the FDA is able to validate the data.

Sponsors of clinical trials are required to make public certain information about active clinical trials and trial results by posting the information on government or independent websites, such as http://clinicaltrials.gov. Clinical testing is typically performed in three phases.

In Phase 1, the drug is administered to a small number of human subjects to confirm its safety and to develop detailed profiles of its pharmacological and pharmacokinetic actions (i.e., absorption, distribution, metabolism, and excretion). Although Phase 1 trials typically are conducted in healthy human subjects, in some instances (including, for example, with some cancer therapies) the study subjects are patients with the targeted disease or condition.

In Phase 2, the drug is administered to groups of patients (usually no more than several hundred) to develop initial data regarding efficacy against the targeted disease and determine the requisite dose and dose intervals, and generate additional information regarding the drug’s safety. In a typical development program, additional animal toxicology studies precede this phase. In some cases, the trial can be split into Phase 2a and 2b studies in order to test smaller subject pools. Some Phase 1 clinical studies may proceed in parallel with some Phase 2 studies.

In Phase 3, the drug is administered to a larger group of patients (usually from several hundred to several thousand or more). Phase 3 studies also may include patients with concomitant diseases and medications. Larger patient populations are evaluated in Phase 3 at multiple study sites and registration studies may be conducted concurrently for the sake of time and efficiency. The extensive clinical testing is intended to obtain additional information about product safety and effectiveness necessary to evaluate the drug’s overall risk-benefit profile and to provide a basis for physician labeling. Phase 3 data often form the core basis on which the FDA evaluates the product’s safety and effectiveness when considering an application to market the drug.

The study sponsor, the FDA or an IRB may suspend or terminate a clinical trial at any time on various grounds, including a determination that study subjects are being exposed to an unacceptable health risk. Additionally, success in early-stage clinical trials does not assure success in later-stage clinical trials, and data from clinical trials are not always conclusive and may be subject to alternative interpretations that could delay, limit or prevent approval.

NDA Submission and Review. After completing the clinical studies, a sponsor seeking approval to market a drug in the United States submits to the FDA a New Drug Application (“NDA”). The NDA is a comprehensive, multi-volume application intended to demonstrate the product’s safety and effectiveness and includes, among other things, pre-clinical and clinical data, information about the drug’s composition, the sponsor’s plans for manufacturing and packaging and proposed labeling. When an NDA is submitted, the FDA makes an initial determination as to whether the application is sufficiently complete to be accepted for review. If the application is not, the FDA may refuse to accept the NDA for filing and request additional information. A refusal to file, which requires resubmission of the NDA with the requested additional information, delays review of the application.

FDA performance goals regarding the timeliness of NDA review generally provide for action on an NDA within 12 months of its submission. That deadline can be extended under certain circumstances, including by the FDA’s requests for additional information. The targeted action date can also be shortened to eight months after submission for products that are granted priority review designation because they are intended to treat serious or life-threatening conditions and demonstrate the potential to address unmet medical needs. Additionally, the FDA has programs for enhanced communication and consultation and other steps to expedite development and review of such products. For example, the Fast Track program is intended to facilitate the development and review of new drugs that demonstrate the potential to address unmet medical needs involving serious or life-threatening diseases or conditions. If a drug receives Fast Track designation, the FDA may review sections of the NDA on a rolling basis, rather than requiring the entire application to be submitted to begin the review. Products with Fast Track designation also may be eligible for more frequent meetings and correspondence with the FDA about the product’s development. Other FDA programs intended to expedite development and review include Accelerated Approval, which allows approval on the basis of a surrogate endpoint that is reasonably likely to predict clinical benefit and Breakthrough Therapy designation, which is available for drugs under development for serious or life-threatening conditions and where preliminary clinical evidence shows that the drug may have substantial improvement on at least one clinically significant endpoint over available therapy. If a drug receives Breakthrough Therapy designation, it will be eligible for all of the benefits of Fast Track designation, as well as for more intensive guidance from the FDA on an efficient drug development program and a commitment from the agency to involve senior FDA managers in such guidance. Even if a product qualifies for Fast Track designation or Breakthrough Therapy designation, the FDA may later decide that the product no longer meets the conditions for designation, and/or may determine that the product does not meet the standards for approval. We anticipate, but cannot ensure, that our product candidates will qualify for such programs.

If it concludes that an NDA does not meet the regulatory standards for approval, the FDA typically issues a Complete Response letter, which communicates the reasons for the agency’s decision not to approve the application and may request additional information, including additional clinical data. An NDA may be resubmitted with the deficiencies addressed, but that does not guarantee approval. Data from clinical trials are not always conclusive, and the FDA’s interpretation of data may differ from the sponsor’s. Obtaining approval can take years, requires substantial resources and depends on a number of factors, including the severity of the targeted disease or condition, the availability of alternative treatments, and the risks and benefits demonstrated in clinical trials. Additionally, as a condition of approval, the FDA may impose restrictions that could affect the commercial prospects of a product, such as a Risk Evaluation and Mitigation Strategy, and could require post-approval commitments to conduct additional studies or conduct surveillance programs to monitor the drug’s effects.

Moreover, once a product is approved, information about its safety or effectiveness from broader clinical use may limit or prevent successful commercialization, either because of regulatory action or market forces. Post-approval modifications to a drug product, such as changes in indications, labeling or manufacturing processes or facilities, may require development and submission of additional information or data in a new or supplemental NDA, which would also require FDA approval.

One of our drug candidates, RX-0201 is an antisense oligonucleotide (“ASO”) compound. To date, the FDA has not approved any NDAs for any ASO compounds for cancer treatment; however, the FDA has approved the ASO compounds fomivirsen (marketed as Vitravene®) as a treatment for cytomegalovirus retinitis, and mipomersen sodium (marketed as Kynamro®), as a treatment for homozygous familial hypercholesterolemia. In addition, RX-0201 is in a drug class known as Akt-1 inhibitors, and drugs from this class have not been approved by the FDA to date.

We have not submitted an NDA for any of our drug candidates.

Exclusivity and Patent Protection. In the United States and elsewhere, certain regulatory exclusivities and patent rights can provide an approved drug product with protection from certain competitors’ products for a period of time and within a certain scope. In the United States, those protections include exclusivity under the Orphan Drug Act, which is available for drugs intended to treat rare diseases or conditions, which generally are diseases or conditions that affect fewer than 200,000 persons in the United States. If a sponsor demonstrates that a drug is intended to treat a rare disease or condition and meets other qualifying criteria, the FDA grants orphan drug designation to the product for that use. A product that has received orphan drug designation is eligible for research and development tax credits and is exempt from user fees under certain circumstances. Additionally, a drug that is approved for its orphan-designated indication generally receives seven years of orphan drug exclusivity. During that period, the FDA generally may not approve any other application for a product containing the same active moiety and proposed for the same indication. There are exceptions, however, most notably when the later product is shown to be clinically superior to the product with exclusivity. An approved orphan drug also may qualify for an exemption from the branded prescription drug fee. Products that qualify for orphan designation may also qualify for other FDA programs that are intended to expedite the development and approval process and, as a practical matter, clinical trials for orphan products may be smaller, simply because of the smaller patient population. Nonetheless, the same approval standards apply to orphan-designated products as for other drugs.

RX-0201 has received orphan drug designation from the FDA for RCC, glioblastoma, ovarian cancer, stomach cancer and pancreatic cancer. RX-3117 received orphan drug designation for pancreatic cancer from the FDA in September 2014.

A medicinal product may be granted an orphan designation in the EU if: (i) it would be used to treat or prevent a life-threatening or chronically debilitating condition and either affects no more than five in 10,000 people in the EU or for economic reasons would be unlikely to be developed without incentives; and (ii) no satisfactory method of diagnosis, prevention or treatment of the condition concerned exists, or, if such a method exists, the medicinal product would be of significant benefit to those affected by the condition. The application for orphan designation must be submitted to the European Medicines Agency (“EMA”) and approved prior to market authorization. Once authorized, orphan medicinal products are entitled to ten years of market exclusivity. During this ten-year period, with limited exceptions, neither the competent authorities of the EU Member States, the EMA, nor the EC are permitted to accept applications or grant marketing authorization for other similar medicinal products with the same therapeutic indication. However, marketing authorization may be granted to a similar medicinal product with the same orphan indication during that period with the consent of the holder of the marketing authorization or if the manufacturer of the product is unable to supply sufficient quantities. Marketing authorization may also be granted to a similar medicinal product with the same orphan indication if the latter product is safer, more effective or otherwise clinically superior to the original product. The period of market exclusivity may be reduced to six years if it can be demonstrated on the basis of available evidence that the original orphan medicinal product is sufficiently profitable not to justify maintenance of market exclusivity.

RX-3117 received orphan designation from the EC in January 2018.

Generic Competition. Any drug candidates approved for commercial marketing under an NDA would be subject to the provisions of the Drug Price Competition and Patent Term Restoration Act of 1984, known as the Hatch-Waxman Act. Among other things, the Hatch-Waxman Act establishes two abbreviated approval pathways for drug products that are in some way follow-on versions of already approved NDA products, including generic versions of the approved product, which may be approved under an Abbreviated New Drug Application by a showing that the generic product is the “same as” the approved product in key respects. Those abbreviated approval pathways generally are available, however, after expiration of certain periods of regulatory exclusivity and/or extended patent protection for the approved NDA product, which the Hatch-Waxman Act also provides. These protections include: (1) five years of regulatory exclusivity for a new chemical entity (generally, the first approval of a product containing a particular active moiety), during which an application for a follow-on product cannot be reviewed; (2) three years of exclusivity for the approval of an NDA or supplemental NDA that contains data from new clinical investigations that were necessary for approval, during which the follow-on product may not receive final approval; and (3) up to five years’ extension of the term of a patent covering a drug that contains an active ingredient not previously approved. The Hatch-Waxman Act also provides a means for the sponsor of an approved NDA to act before approval of a proposed abbreviated NDA to sue to protect patents claiming the drug substance, drug product, or an approved method of using the drug. The laws of other key markets likewise create both opportunities for exclusivity periods and patent protections and the possibility of generic competition once such periods or protections have either expired or have been successfully challenged by generic entrants.

Post-Approval Regulation

Once approved, products are subject to continuing extensive regulation by the FDA. If ongoing regulatory requirements are not met, or if safety problems occur after a product reaches market, the FDA may take actions to change the conditions under which the product is marketed, including suspending or even withdrawing approval. In addition to FDA regulation, the healthcare industry, and therefore our business, is also subject to extensive federal, state, local and foreign regulation.

Good Manufacturing Practices. Companies engaged in manufacturing drug products or their components must comply with applicable current Good Manufacturing Practice (“cGMP”) requirements, which include requirements regarding organization and training of personnel, building and facilities, equipment, control of components and drug product containers, closures, production and process controls, packaging and labeling controls, holding and distribution, laboratory controls and records and reports. The FDA inspects equipment, facilities and manufacturing processes before approval and conducts periodic re-inspections after approval. Failure to comply with applicable cGMP requirements or the conditions of the product’s approval may lead the FDA to take administrative enforcement action. Although we periodically monitor FDA compliance of the third parties on which we rely for manufacturing our drug products, we cannot be certain that our present or future third-party manufacturers will consistently comply with cGMP or other applicable FDA regulatory requirements.

Sales and Marketing. Once a product is approved, its advertising, promotion and marketing will be subject to close regulation, including with regard to promotion to healthcare practitioners, direct-to-consumer advertising, communications regarding unapproved uses, industry-sponsored scientific and educational activities and promotional activities involving the internet. In addition to FDA restrictions on marketing of pharmaceutical products, state and federal fraud and abuse laws have been applied to restrict certain marketing practices in the pharmaceutical industry for many years. Some of the pertinent laws are open to a variety of interpretations. In addition, these laws and their interpretations are subject to change.

Other Requirements. Companies that manufacture or distribute drug products pursuant to approved NDAs must meet numerous other regulatory requirements, including adverse event reporting, submission of periodic reports, and record-keeping obligations.

Fraud and Abuse Laws. At such time as we market, sell and distribute any products for which we obtain marketing approval, it is possible that our business activities could be subject to scrutiny and enforcement under one or more federal or state health care fraud and abuse laws and regulations, which could affect our ability to operate our business. These restrictions under applicable federal and state health care fraud and abuse laws and regulations that may affect our ability to operate include:

| · |

The federal Anti-Kickback Law, which prohibits, among other things, knowingly or willingly offering, paying, soliciting or receiving remuneration, directly or indirectly, in cash or in kind, to induce or reward the purchasing, leasing, ordering or arranging for or recommending the purchase, lease or order of any health care items or service for which payment may be made, in whole or in part, by federal healthcare programs such as Medicare and Medicaid. This statute has been interpreted to apply to arrangements between pharmaceutical companies on one hand and prescribers, purchasers and formulary managers on the other. Further, the Affordable Care Act clarified among other things that liability may be established under the federal Anti-Kickback Law without proving actual knowledge of the statute or specific intent to violate it. In addition, the Affordable Care Act amended the Social Security Act to provide that the government may assert that a claim including items or services resulting from a violation of the federal Anti-Kickback Law constitutes a false or fraudulent claim for purposes of the federal civil False Claims Act. Although there are a number of statutory exemptions and regulatory safe harbors to the federal Anti-Kickback Law protecting certain common business arrangements and activities from prosecution or regulatory sanctions, the exemptions and safe harbors are drawn narrowly, and practices that do not fit squarely within an exemption or safe harbor, or for which no exception or safe harbor is available, may be subject to scrutiny;

|

| · |

The federal civil False Claims Act, which prohibits, among other things, individuals or entities from knowingly presenting, or causing to be presented, a false or fraudulent claim for payment of government funds or knowingly making, using or causing to be made or used, a false record or statement material to an obligation to pay money to the government or knowingly concealing or knowingly and improperly avoiding, decreasing or concealing an obligation to pay money to the federal government. Many pharmaceutical and other healthcare companies have been investigated and have reached substantial financial settlements with the federal government under the civil False Claims Act for a variety of alleged improper marketing activities, including: providing free product to customers with the expectation that the customers would bill federal programs for the product; providing sham consulting fees, grants, free travel and other benefits to physicians to induce them to prescribe the company’s products; and inflating prices reported to private price publication services, which are used to set drug payment rates under government healthcare programs. In addition, in recent years the government has pursued civil False Claims Act cases against a number of pharmaceutical companies for causing false claims to be submitted as a result of the marketing of their products for unapproved, and thus non-reimbursable, uses. Pharmaceutical and other healthcare companies also are subject to other federal false claim laws, including, among others, federal criminal healthcare fraud and false statement statutes that extend to non-government health benefit programs;

|

| · |

Analogous state laws and regulations, such as state anti-kickback and false claims laws, may apply to items or services reimbursed under Medicaid and other state programs or, in several states, apply regardless of the payor. Some state laws also require pharmaceutical companies to report expenses relating to the marketing and promotion of pharmaceutical products and to report gifts and payments to certain healthcare providers in the states. Other states prohibit providing meals to prescribers or other marketing related activities. In addition, California, Connecticut, Nevada and Massachusetts require pharmaceutical companies to implement compliance programs or marketing codes of conduct.

|

| · |

The federal Physician Payment Sunshine Act, being implemented as the Open Payments Program, requires certain pharmaceutical manufacturers to engage in extensive tracking of payments and other transfers of value to physicians and teaching hospitals, and to submit such data to the Centers for Medicare and Medicaid Services (“CMS”), which will then make all of this data publicly available on the CMS website. Pharmaceutical manufacturers with products for which payment is available under Medicare, Medicaid or the State Children’s Health Insurance Program are required to track reportable payments and must submit a report to CMS on or before the 90th day of each calendar year disclosing reportable payments made in the previous calendar year. Failure to comply with the reporting obligations may result in civil monetary penalties;

|

| · |

The federal Foreign Corrupt Practices Act of 1997 and other similar anti-bribery laws in other jurisdictions generally prohibit companies and their intermediaries from providing money or anything of value to officials of foreign governments, foreign political parties, or international organizations with the intent to obtain or retain business or seek a business advantage. Recently, there has been a substantial increase in anti-bribery law enforcement activity by U.S. regulators, with more frequent and aggressive investigations and enforcement proceedings by both the Department of Justice and the U.S. Securities and Exchange Commission (the “SEC”). Violations of United States or foreign laws or regulations could result in the imposition of substantial fines, interruptions of business, loss of supplier, vendor or other third-party relationships, termination of necessary licenses and permits and other legal or equitable sanctions. Other internal or government investigations or legal or regulatory proceedings, including lawsuits brought by private litigants, may also follow as a consequence.

|

Violations of any of the laws described above or any other governmental regulations are punishable by significant civil, criminal and administrative penalties, damages, fines and exclusion from government-funded healthcare programs, such as Medicare and Medicaid. Although compliance programs can mitigate the risk of investigation and prosecution for violations of these laws, the risks cannot be entirely eliminated. Moreover, achieving and sustaining compliance with applicable federal and state privacy, security and fraud laws may prove costly.

Privacy Laws. We are also subject to laws and regulations covering data privacy and the protection of health-related and other personal information. The legislative and regulatory landscape for privacy and data protection continues to evolve, and there has been an increasing focus on privacy and data protection issues which may affect our business, including recently enacted laws in all jurisdictions where we operate. Numerous federal and state laws, including state security breach notification laws, state health information privacy laws and federal and state consumer protection laws, govern the collection, use and disclosure of personal information. Failure to comply with such laws and regulations could result in government enforcement actions and create liability for us (including the imposition of significant penalties), private litigation and/or adverse publicity that could negatively affect our business. In addition, if we successfully commercialize our drug candidates, we may obtain patient health information from healthcare providers who prescribe our products and research institutions we collaborate with, and they are subject to privacy and security requirements under the Health Insurance Portability and Accountability Act of 1996, as amended by the Health Information Technology for Economic and Clinical Health Act (“HIPAA”). Although we are not directly subject to HIPAA other than with respect to providing certain employee benefits, we could potentially be subject to criminal penalties if we knowingly obtain or disclose individually identifiable health information maintained by a HIPAA-covered entity in a manner that is not authorized or permitted by HIPAA.

Coverage and Reimbursement

Significant uncertainty exists as to the coverage and reimbursement status of any drug candidates for which we may obtain regulatory approval. The regulations that govern marketing approvals, pricing and reimbursement for new drug products vary widely from country to country. Current and future legislation may significantly change the approval requirements in ways that could involve additional costs and cause delays in obtaining approvals. Some countries require approval of the sale price of a drug before it can be marketed. In many countries, the pricing review period begins after marketing or product licensing approval is granted. In some foreign markets, prescription pharmaceutical pricing remains subject to continuing governmental control even after initial approval is granted. As a result, we might obtain marketing approval for a product in a particular country, but then be subject to price regulations that delay our commercial launch of the product, possibly for lengthy time periods, which could negatively impact the revenues we are able to generate from the sale of the product in that particular country. Adverse pricing limitations may hinder our ability to recoup our investment in one or more product candidates even if our product candidates obtain marketing approval.

Our ability to commercialize any products successfully also will depend in part on the extent to which coverage and adequate reimbursement for these products and related treatments will be available in a timely manner from government third-party payors, including government healthcare programs such as Medicare and Medicaid, commercial health insurers and managed care organizations. Government authorities and other third-party payors, such as private health insurers and health maintenance organizations, determine which medications they will cover and establish reimbursement levels. Third-party payors may limit coverage to specific products on an approved list, or formulary, which may not include all of the FDA-approved products for a particular indication. The process for determining whether a payor will provide coverage for a product may be separate from the process for setting the price or reimbursement rate that the payor will pay for the product once coverage is approved.

A primary trend in the U.S. healthcare industry and elsewhere is cost containment. Government healthcare programs and other third-party payors are increasingly challenging the prices charged for medical products and services and examining the medical necessity and cost-effectiveness of medical products and services, in addition to their safety and efficacy, and have attempted to control costs by limiting coverage and the amount of reimbursement for particular medications. Increasingly, third-party payors are requiring that drug companies provide them with predetermined discounts from list prices and are challenging the prices charged for medical products. We cannot be sure that coverage and reimbursement will be available promptly or at all for any product that we commercialize and, if reimbursement is available, what the level of reimbursement will be. Moreover, eligibility for coverage and reimbursement does not imply that any drug will be paid for in all cases. Limited coverage may impact the demand for, or the price of, any product candidate for which we obtain marketing approval. If coverage and reimbursement are not available or reimbursement is available only to limited levels, we may not successfully commercialize any product candidate for which we obtain marketing approval.

Payors also are increasingly considering new metrics as the basis for reimbursement rates, such as average sales price (“ASP”), average manufacturer price (“AMP”) and actual acquisition cost. The existing data for reimbursement based on these metrics is relatively limited, although certain states have begun to survey acquisition cost data for the purpose of setting Medicaid reimbursement rates. CMS surveys and publishes retail community pharmacy acquisition cost information in the form of National Average Drug Acquisition Cost (“NADAC”) files to provide state Medicaid agencies with a basis of comparison for their own reimbursement and pricing methodologies and rates. It may be difficult to project the impact of these evolving reimbursement mechanics on the willingness of payors to cover our products for which we receive regulatory approval.

If we successfully commercialize any of our products, we may participate in the Medicaid Drug Rebate Program. Participation is required for federal funds to be available for our products under Medicaid and Medicare Part B. Under the Medicaid Drug Rebate Program, we would be required to pay a rebate to each state Medicaid program for our covered outpatient drugs that are dispensed to Medicaid beneficiaries and paid for by a state Medicaid program as a condition of having federal funds being made available to the states for our drugs under Medicaid and Part B of the Medicare program.

Federal law requires that any company that participates in the Medicaid Drug Rebate Program also participate in the Public Health Service’s 340B drug pricing program in order for federal funds to be available for the manufacturer’s drugs under Medicaid and Medicare Part B. The 340B drug pricing program requires participating manufacturers to agree to charge statutorily-defined covered entities no more than the 340B “ceiling price” for the manufacturer’s covered outpatient drugs. These 340B covered entities include a variety of community health clinics and other entities that receive health services grants from the Public Health Service, as well as hospitals that serve a disproportionate share of low-income patients.

In addition, in order to be eligible to have its products paid for with federal funds under the Medicaid and Medicare Part B programs and purchased by the Department of Veterans Affairs (the “VA”), Department of Defense (“DoD”), Public Health Service, and Coast Guard (the “Big Four agencies”) and certain federal grantees, a manufacturer also must participate in the VA Federal Supply Schedule (“FSS”) pricing program, established by Section 603 of the Veterans Health Care Act of 1992 (the “VHCA”). Under this program, the manufacturer is obligated to make its covered drugs (innovator multiple source drugs, single source drugs, and biologics) available for procurement on an FSS contract and charge a price to the Big Four agencies that is no higher than the Federal Ceiling Price (“FCP”), which is a price calculated pursuant to a statutory formula. The FCP is derived from a calculated price point called the “non-federal average manufacturer price” (“Non-FAMP”), which we will be required to calculate and report to the VA on a quarterly and annual basis. Moreover, pursuant to Defense Health Agency (“DHA”) regulations, manufacturers must provide rebates on utilization of their innovator and single source products that are dispensed to TRICARE beneficiaries by TRICARE network retail pharmacies. The formula for determining the rebate is established in the regulations and is based on the difference between the annual non-federal average manufacturer price and the Federal Ceiling Price, each required to be calculated by us under the VHCA. The requirements under the 340B, FSS, and TRICARE programs could reduce the revenue we may generate from any products that are commercialized in the future and could adversely affect our business and operating results.